Investing in rental properties has long been a wealth-building strategy, but traditional long-term rentals often limit cash flow due to market rates, vacancies, and single-tenant risks. Enter PadSplit, a unique coliving model designed to maximize rental income while providing affordable workforce housing to meet growing demand.

Unlike traditional coliving spaces that cater to short-term or luxury renters, PadSplit operates as an affordable, long-term shared housing solution where residents rent private, furnished rooms in a shared home with weekly payments, no deposits, and all utilities included. For investors, this means higher occupancy rates, lower turnover, and up to 30% higher returns compared to standard rentals.

PadSplit properties offer real estate investors an opportunity to generate strong rental income while providing affordable housing solutions. Here’s what you need to know about financing these coliving investments.

Investor success story: How one PadSplit property generates 2X market rent

Take the case of Peter Pasternack, a lead character from A&E’s “Flip This House” and a successful real estate investor in Atlanta, Georgia, who converted a rental property into a PadSplit. With Airbnb, he was earning $2,500 per month in rent. However, after converting it into a coliving duplex, his monthly revenue increased to $4,600.

Why more investors are turning to coliving

Here’s what makes PadSplit properties an attractive investment opportunity:

Higher Returns – 30% higher returns compared to traditional rentals.

Strong Demand – Consistent demand due to affordable housing shortage

Operational Flexibility – Flexible management to maximize profits

Now, let’s explore how to secure funding.

Top loan options available for PadSplit coliving properties

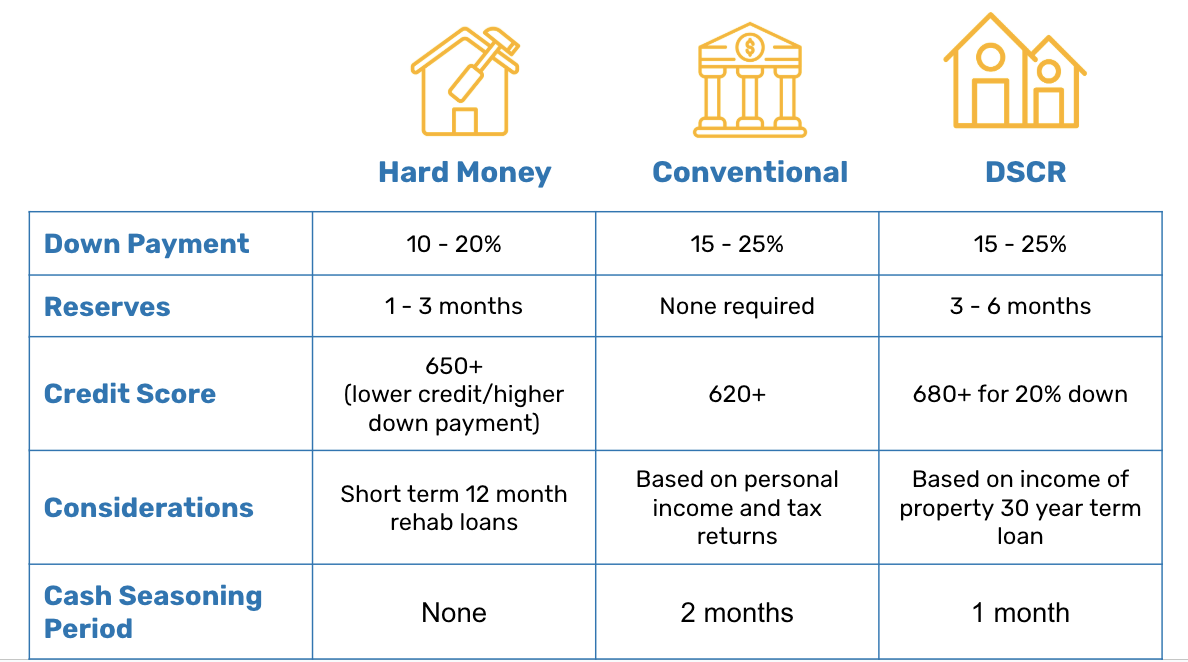

1. DSCR Loans: The Go-To Option for Coliving Investments

DSCR loans are popular for financing co-living properties since they focus on the property’s projected income rather than your personal earnings. These loans are specifically designed for investment properties like PadSplit homes.

- Interest rate: Typically 1% higher than conventional loans.

- Down Payment: Typically 20-25% of the purchase price.

- Loan Approval: Lenders evaluate if your projected rental income will be sufficient to make monthly mortgage payments.

- Best For: Property investors whose expected rental income exceeds personal earnings.

Down Payment Options for PadSplit Properties

You can fund your down payment through personal savings or by leveraging home equity through a HELOC.

2. Conventional Loans: Traditional Financing with Income Verification

Conventional loans can be an option for financing PadSplit properties, though they require proof of personal income and tax returns. Unlike DSCR loans, which focus on rental income, conventional loans are based on the borrower’s financial standing.

- Down payment: Typically 20%.

- Reserves Required: None.

- Approval Process: Based on personal income, tax returns, and creditworthiness.

- Seasoning Period: Requires two months of cash seasoning before approval.

- Best For: Investors with strong personal income and financial documentation.

3. Hard Money Loans: Quick for Short-Term Debt

Hard money loans offer quick financing for property purchases and renovations, making them suitable for converting homes into PadSplit spaces. However, these loans come with 8-12% interest rates and short 6-24 month terms.

Best for experienced investors who:

- Need rapid funding for properties requiring renovation.

- Have a clear strategy to refinance into a DSCR loan after stabilization.

4. Reducing Risk Through Strategic Partnerships

For first-time PadSplit investors, partnering with experienced professionals offers significant advantages:

Strategic Benefits

- Split costs and share expertise through joint ventures.

- Access reliable market data for informed decisions.

- Leverage established contractor and vendor networks.

💡 Tip: Consider connecting with PadSplit’s team to explore financing partnerships and identify promising markets. Their experience can help guide your investment strategy.

5. Test the Waters: Lease-First Strategy

Consider leasing before buying to explore PadSplit’s potential with lower risk:

- Start with a 2-year lease to evaluate the co-living model.

- Avoid large down payments while testing market viability.

- Maintain flexibility with traditional rental backup options.

While you might face small monthly losses if performance falls short, this approach limits exposure compared to direct property ownership.

Potential Lenders for Financing a PadSplit Property

Finding the right lender is essential for successfully financing your PadSplit investment. The following lenders specialize in DSCR loans, hard money loans, and other financing options suitable for coliving properties:

Hard Money Loan:

- Backflip

- Nexa Mortgage

- Fernando Corona

Long Term Debt:

- Coast2Coast Mortgage, Jeffrey Weller – (904) 500-LOAN (5626), www.PadSplitLoans.com

- Fernando Corona

- Kimberlee Bellamy

Alternative financing strategies

Smart investors recognize the value of exploring diverse financing paths beyond conventional loans. Here’s a comprehensive look at alternative ways to fund your PadSplit investment.

Seller financing

Working directly with property owners can create mutually beneficial arrangements. This approach offers:

- Flexible down payment and interest rate negotiations

- Reduced closing costs and paperwork

- Faster closing timelines without traditional bank requirements

- Opportunity to build relationship-based investment partnerships

Retirement account strategies

Self-directed IRAs provide a powerful vehicle for real estate investment:

- Tax-advantaged real estate purchases within retirement accounts

- Ability to diversify retirement portfolios beyond traditional assets

- Option to combine IRA funds with other financing methods

- Potential for tax-deferred or tax-free returns depending on account type

Collaborative funding approaches

Modern investment platforms and partnerships expand financing possibilities:

- Real estate crowdfunding platforms connect multiple investors

- Private lending arrangements with experienced real estate investors

- Joint venture partnerships to combine resources and expertise

- Syndication opportunities for larger-scale investments

Each financing strategy carries unique advantages and considerations. Success often comes from matching the right financing approach with your investment goals, timeline, and risk tolerance.

Managing investment risk in PadSplit properties

When considering a PadSplit investment, understanding and addressing potential risks is crucial for long-term success. Let’s explore key concerns and practical mitigation strategies.

Occupancy management

High demand for affordable housing typically drives strong occupancy rates in PadSplit properties. However, prudent investors should:

- Build financial models using conservative vacancy estimates that account for market fluctuations

- Regularly assess local market conditions to maintain competitive weekly rates

- Implement professional property management practices, including thorough member screening and responsive maintenance

- Maintain property quality to encourage longer stays and positive member reviews

Regulatory compliance

Each jurisdiction has unique requirements for shared housing. To ensure compliance:

- Research local zoning laws and housing regulations before property acquisition

- Engage qualified real estate attorneys familiar with shared housing regulations

- Connect with experienced PadSplit investors in your target market

- Stay informed about regulatory changes that could affect your investment

Financial planning

Understanding the cost structure helps create realistic profit projections:

- Fixed costs include property taxes, insurance, and regular maintenance

- Variable expenses cover utilities, cleaning services, and member turnover

- Weekly payment model provides consistent cash flow and helps offset operating costs

- Lower turnover rates compared to traditional rentals reduce vacancy-related expenses

- Emergency fund maintenance ensures resources for unexpected repairs

When managed effectively, these potential challenges can be transformed into opportunities for sustainable returns while providing essential affordable housing solutions.

Choosing your right financing path

The right financing approach for your PadSplit property depends on your investment goals and risk tolerance. Consider these options:

- DSCR loans provide stable long-term financing based on rental income potential

- Hard money loans enable quick purchases and renovations at premium rates

- Strategic partnerships offer shared resources and expert guidance

- The lease-first strategy allows market testing with minimal upfront investment

Ready to explore PadSplit investments? Connect with our team to discuss financing options and develop your investment strategy. Visit PadSplit.com today.

The information provided in this blog post is for general informational purposes only. It should not be construed as legal, financial, or professional advice. The content is intended to provide general guidance and should not be relied upon for making specific decisions.

PadSplit strongly recommends consulting with qualified legal counsel, licensed financial advisors, tax professionals, or other relevant experts for advice concerning your specific situation and investment needs. PadSplit makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, or suitability of the information contained in this post.